NG/LNG – This Week's Main Drivers and the Look Ahead | 6.21.26

- Timothy Beggans

- Jun 21

- 2 min read

This Week's Main Drivers:

Natural gas and LNG markets navigated a mix of bullish supply disruptions and easing geopolitical risks this week.

The biggest headline came from the Middle East as Iran-related negotiations moved toward a tentative agreement and shipping traffic through the Strait of Hormuz resumed normal operations after recent disruptions. The reduced geopolitical risk premium weighed on global gas prices.

In the U.S., LNG demand strengthened as Golden Pass LNG continued commissioning activities, with Train 1 reportedly reaching roughly 50% utilization. Meanwhile, Tropical Storm Arthur formed in the Gulf of America, adding another variable as hurricane season begins.

Weather remained a key driver. Extreme heat and humidity pushed ERCOT to a new June peak-load record while South Texas Project Nuclear Unit 2 unexpectedly tripped offline, increasing near-term gas-fired generation demand.

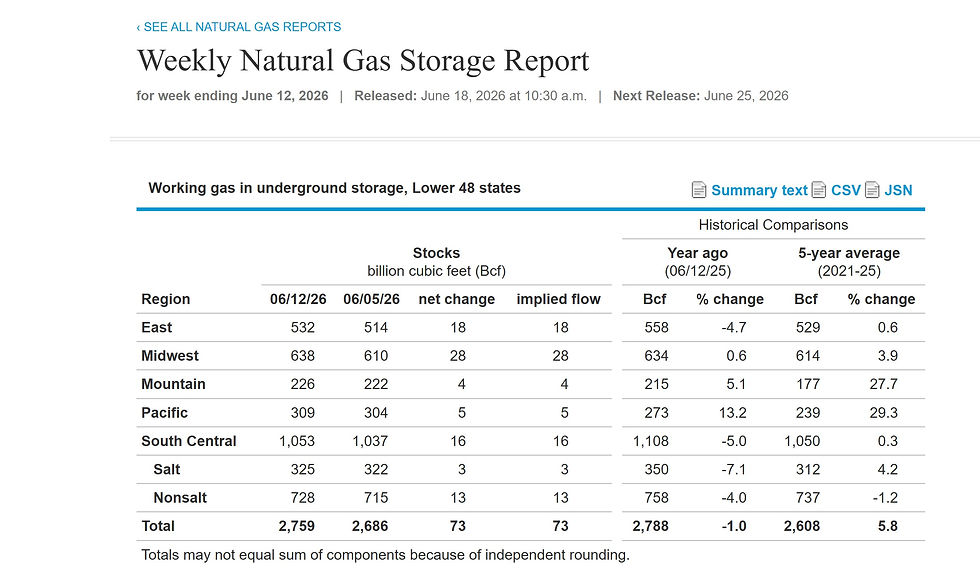

The EIA reported a +73 Bcf storage injection, matching the five-year average and significantly below last year's +97 Bcf build. The report was viewed as supportive, particularly given elevated cooling demand across much of the country.

Internationally, Qatar continued loading LNG cargoes from Ras Laffan while labor action at Australia's Ichthys LNG facility was extended through July 6, keeping supply concerns on traders' radar. Longer term, developing El Niño conditions could influence both Atlantic hurricane activity and North American weather patterns later this year.

The Look Ahead:

Attention now shifts toward structural LNG market developments.

Delfin LNG reached FID on the first U.S. floating LNG export project, highlighting continued confidence in long-term LNG demand growth. Reports also indicate ExxonMobil is evaluating global LNG acquisition opportunities as competition for future supply intensifies.

Spot LNG economics increasingly favor Asia, encouraging Atlantic Basin cargoes to move eastward. At the same time, European gas storage remains below historical norms for this point in the injection season, maintaining competition for LNG volumes despite softer industrial demand.

As the U.S. approaches the July 4 holiday period, domestic natural gas demand may temporarily soften from reduced industrial activity. However, summer cooling demand, LNG feedgas growth, hurricane season risks, and global supply disruptions continue to provide support beneath the market.

The key question remains whether growing LNG demand and weather-driven power burns can offset seasonal storage injections as summer progresses.

Links:

Comments